BoE gilt purchase Traders sold their holdings after the Bank of England confirmed it would not extend the deadline for its bond buying program this week.

And hours later, everything in the market turned upside down. The BOE made the largest contingency purchases since the response began last month. It made a total of £4.56 billion ($5.1 billion) on Wednesday by buying all traditional bonds offered by investors. It wiped out almost all 30 years of losses and ended the day with 4.8% essentially unchanged.

The BOE has increasingly intervened to maintain financial stability. This week, it increased the amount of gilt it can buy in a given operation and expanded purchases to inflation-linked debt after a record sale.

In the background, investors are worried that the withdrawal of BOE support will throw the market into more turmoil, and pension funds are calling for expansion of the measures. On Wednesday, the central bank was forced to reiterate that its bond purchases will end this week, surprising some traders after the Financial Times specifically briefed bankers that officials could extend the deadline.

US bonds and global bond sales US Treasuries and other sovereign debt fell with equity markets this year as central banks around the world raised interest rates to curb inflation and increased yields on government bonds that moved against prices. Infrequent liquidity events in the Treasury market exacerbated price fluctuations, keeping some investors on the sidelines.

.png)

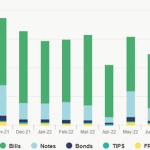

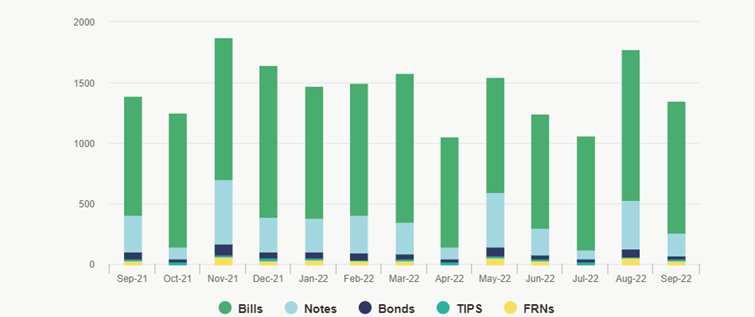

US Treasury Securities Issue ($B)

September 22 Bonds = $30 billion

YTD statistics include:

Issuance (as of September) $12.5 trillion, Y/Y -15.1%

Transactions (as of September) ADV 627.0 bn, 2.0% Y/Y

$23.7 trillion in circulation (as of September), Y/Y +8.3%

US bonds and worldwide correlation

“Central banks around the world are battling a common enemy and using largely the same tools. As a result, we see significantly high correlations between bond markets,“ said Andy Sparks, head of portfolio management research at MSCI.

.jpg)

Correlation of bond yields of some countries with US Treasuries since 2015… Correlations related to currency-adjusted yields. A correlation of 1 means that the assets are moving in the same direction. -1 means assets are moving in opposite directions.

BOJ intervention As part of the pandemic stimulus, the BOJ increased government bonds by Yen 48 trillion – less than half of the increase in loans. And it stopped increasing its holdings in early 2021, and then allowed its assets to decrease by 11 trillion yen over the next 12 months through February 2022. So even while the credit portion of his QE was still bobbing up and down, his QE had bond portions.

But then, in early 2022, the Fed started raising rates and going ahead with the idea of QT, the ECB started talking about rate hikes, and while other central banks had been raising rates for months, the BOJ was still holding on to its negative.

And investors started dumping the JGBs and the yield was hitting the yield stabilizer, and the BOJ decided to defend the yield fixed with real purchases as well, mostly with the rhetoric of “unlimited” bond purchases that was widely circulated in the financial media. Its assets increased by 18 trillion yen, taking back 11 trillion yen in QT and adding 7 trillion yen to it. It wasn’t a huge amount, but it was large enough to justify the yield curve:

.jpg)

BOJ Assets: Government Securities (tri trillion, monthly)

Defending currencies and controlling yield curves In the UK, bank intervention without consulting the Monetary Policy Committee (MPC) is a form of what is known as yield curve control. This is a variant of QE where the central bank wants to generate a certain return rather than creating a certain amount of money to buy bonds. Such a policy is mainly associated with Japan, where the central bank has purchased bonds since 2016 to keep yields at very low levels.

So far, the Bank of Japan has achieved its goal, but the yen has lost a lot of value as the bank needs to create more money through QE: there are currently US$3.8 trillion in Japanese government bonds, more than half of the total market.

“Given how Japanese government bond yields are an anchor for global fixed income, the repercussions of a policy change are likely to reverberate far in global assets,” UBS strategists including Rohan Khanna wrote this week: “Markets most affected by the BOJ policy change will be the markets with the largest footprint of Japanese investors.”

While an imminent policy change isn’t on UBS’s radar, a team at the bank reviewed the possible implications of a surprise move this week as part of a memo answering “the toughest customer questions.”

For example, raising the upper bound on the BOJ’s hard stance on 10-year yields “helps erase speculative yen deficits and helps the currency rise to 130 against the dollar,” he said. While not a fundamental scenario, abandoning the BOJ’s cap altogether This could see an increase in US mortgage-backed securities yields, outstripping the large JGBs held by Japanese investors.

Conclusion? While most central banks are heading in the same direction, speculation that a country may give up its fight against inflation can fuel hopes that other policymakers will eventually follow suit, and lead to fluctuations in government debt around the world.

The Bank of England intervention is also likely to put additional downward pressure on the sterling, although the moves by Japan and the UK to control bond yields are slightly different. It will also be inflationary. This shows how unattractive the policy options are at the moment.

We also found that controlling the yield curve as Japan did is not a good tool to control the strength of a currency. As a result of Japan’s actions, the JPY weakened against the USD.

Kaynak Enver Erkan / Tera Yatırım

Hibya Haber Ajansı