Turkey: Inflation and loose policy ground

-Towards a single digit policy rate

-Currency and loan interest proactivity

-The future of macroprudential measures

The CBRT lowered the benchmark interest rates again, and at its subsequent third meeting, signaled that the end of the cuts, which deepened the extremely loose policy cycle after the faster-than-expected interest rate cut, was approaching. Despite the 85.5% annual inflation rate, the Monetary Policy Committee reduced the one-week repo rate from 12% to 10.5%. As extracted from the Central Bank’s policy text, we expect a similar rate cut and single-digit policy rate to be reached at the November meeting.

Consumer price inflation continued to rise in October by increasing by 3.54% on a periodic basis and reached 85.51% from 83.45% on an annual basis. We consider this rate, which is 17 times the 5% medium-term target of the Central Bank, as a possible peak for this year and the 24-year historical series. In addition to the base effects, if the unexpected negative wind effect is not observed, inflation will start to decrease at annual rates in the coming months. We think that the CPI will slow down more slowly than the official expectations and that the most important thing is core inflation and its rigidity. In this framework, we see the inflation rate as 75.7% at the end of the year, according to the latest realizations.

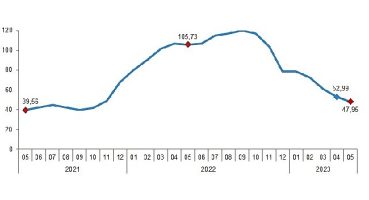

Comparison of CBRT gross, net and net reserves excluding swap… Source: Bloomberg, CBRT, Tera Yatırım

During the week of October 28, the CBRT’s gross reserves increased by 0.2 billion US dollars to 114.4 billion US dollars, while the Bank’s net reserves increased by 1.9 billion US dollars to 13.4 billion US dollars. We should note that the CBRT’s total swap volume increased by USD 1.9 billion that week to reach USD 72 billion. Therefore, the CBRT’s gross reserves increased by USD 3.1 billion year on year and decreased by USD 9.6 billion compared to a year ago; net reserves, on the other hand, increased by USD 5.1 billion year on year and decreased by USD 19.2 billion compared to a year ago.

The BRSA expanded the commercial lira loan ban by lowering the threshold for holding foreign currency assets from 15 million lira to 10 million lira. The regulation in question is the revised version of the limits announced by the BRSA at the beginning of the summer, and the restrictions seem to have become more stringent with the new figures. The basis for such measures by the CBRT and the BRSA is clear; companies with cash or foreign currency are asked not to use loans and to evaluate the cash they have. They will need to reduce their foreign currency cash positions to access credit.

The CBRT, on the other hand, revised the practice of holding securities in lira by increasing the “securities establishment rate” of lenders from 3% to 5%. Although it is seen as one of the frequent and regulatory changes, it is aimed to increase the amount of bonds held by banks. Banks started buying CPI-linked bonds to protect themselves to make a real profit. However, they are directed to low-interest fixed-income debt instruments with securities establishment obligations.

Headline inflation and its main sub-layers… Source: Bloomberg, TURKSTAT, Tera Yatırım

We think that the CBRT’s ongoing rate cut cycle may continue to weaken the lira and feed inflation. On the other hand, we expect the current perspective and growth-oriented approach to be preserved in monetary and fiscal policies, which we expect to remain lax in the run-up to the elections.

Emerging markets: political and geopolitical influences

-Current status of developing economies

-Politics in Brazil

-Russia situation

Emerging market (EM) stocks did not participate in the rally seen in advanced market stocks in October. The MSCI EM Index fell, with China by far the weakest index market. The closely watched 20th Party Congress consolidated President Xi’s mandate and did not signal any near-term decline in the zero Covid policy. New US export controls on the semiconductor industry, which will restrict Chinese companies’ access to advanced chips, also weighed on sentiment. Qatar and Taiwan were other EMs that posted negative returns. Taiwan underperformed, while Qatar’s returns were ahead of the benchmark.

The markets of oil-exporting countries such as Saudi Arabia, UAE and Kuwait finished ahead of the index as oil prices rose with OPEC+’s production cuts. Brazil performed better as its currency strengthened, and electoral volatility ended when former President Lula won a third term. Korea and Mexico also beat the index, with the latter supported by currency gains.

Hungary and Poland, which have performed poorly in recent months, rose to double digits in dollar terms in October and were supported by the strengthening of the exchange rates.

Turkey was the best performing index market of the month. Despite the fact that consumer price index (CPI) inflation reached 83.5% on an annual basis in September, the Central Bank cut the interest rate again, this time to 10.5%, at its meeting in October.

Former Brazilian president and left-wing candidate Luiz Inacio Lula da Silva, known as Lula, defeated incumbent far-right Jair Bolsonaro in the second round of the national elections held in Brazil. The striking political turnaround has been welcomed by environmental, indigenous and progressive activists. Bolsonaro’s presidency has seen deforestation in the Amazon rise to its highest level in 15 years. With 100% of the votes counted in one of the world’s largest democracies (Brazil has 156 million eligible voters), Lula received 50.9% of the votes, versus 49.1% of Bolsonaro. The elected president will take office on January 1, 2023.

Meanwhile, as the war between Russia and Ukraine drifts into autumn and winter, the economic repercussions on both countries and the rest of the world are becoming clearer. Data released by the Russian Ministry of Economic Development on Wednesday showed that the downturn in the country continued in September and continued with a significant contraction.

While Russia insists its economy can withstand the storm of international sanctions, Foreign Minister Sergei Lavrov insisted earlier this week that “no one can stop” Russia’s economy.

Russia has recently made a surprise return to the Black Sea grain initiative, an agreement between Ukraine and Turkey and the UN to secure exports of vital agricultural products such as maize and wheat, of which Russia and Ukraine are the main producers. The Turkish president said that after the revival of the agreement, grain shipments will be given priority to African countries suffering from acute food shortages such as Somalia and Sudan.

Advanced economies: Market transfer mechanism

-Fed’s latest statement and final rate guide (December dot chart expectations): Rate work will be slower but longer

-Approaching recession: freezing winter for Europe

-Market transmission mechanism: Everyone interrupts markets (intervention in currencies, returns)

Investors and strategists are raising expectations about how much the Fed will raise interest rates in an effort to curb inflation, following Wednesday’s hawkish comments from Fed Chairman Jerome Powell. Since Wednesday, futures traders have raised expectations for the Fed’s terminal interest rate – the highest overnight benchmark in the policy tightening cycle – to 5.14% in June 2023.

Fed Rates. Source: Federal Reserve

US-based S&P Global Market Intelligence recently predicted close but relatively short and sharp recessions in the eurozone and the European Union (EU). They expect cumulative real gross domestic product (GDP) losses to exceed 1%, primarily due to weakness in private consumption, as rising inflation affects household real incomes in the region. Energy shortages due to unusually cold weather could lead to much deeper short-term production contractions than anticipated, concentrated in the industrial sector.

Eurozone composite PMI flash forecast fell to 47.1, lower than expected in October. This is not only a 2-year low, but also the fourth consecutive month that the PMI has been in the bearish zone below 50, clearly indicating negative GDP growth. We get the same story from the European Commission’s economic sentiment indicator: October dropped to its lowest level since November 2020 for the eighth month. Forward-looking components of job surveys, such as hiring intentions and new orders, are trending downwards, a sign that the downturn will intensify in the coming months.

Consumption is softening. Source: Refinitiv Datastream.

Admittedly, consumer confidence rose slightly in October, but is close to its historic low reached in September. Households’ intention to make large purchases, renovate or buy a home is very low as they expect higher unemployment in the next 12 months. This strong cooling in consumption is also seen in high-frequency data such as hotel bookings, which declined after summer.

We reiterate our 4Q22 and 1Q23 GDP contraction forecasts. But there is more. The ECB’s current tightening policies and the continued difficult energy transition away from Russian gas will limit the next recovery. After better third-quarter figures, 2022 eurozone growth projections have been revised at the terminal to a median 3.1%. A growth of -0.7% is now expected for 2023 and 1.3% for 2024.

The US Federal Reserve’s aggressive monetary tightening has supported US dollar and US yields in recent months. Faced with the consequences of a strong USD compared to foreign currencies, Japan spent 6,349.9 billion yen on foreign exchange market interventions last month, hitting a monthly record for the country’s yen buying operations.

Guan Tao, former director of the international payments department of the State Foreign Exchange Administration (SAFE), said that currency fluctuations in China did not result in an economic shock or inflation, the market is still regular and financial stability is intact. However, Guan said, “If some speculators go too far, the People’s Bank of China must be stronger than the Bank of Japan (BOJ) to intervene in the foreign exchange market.”

Kaynak: Tera Yatırım-Enver Erkan

Hibya Haber Ajansı