We will probably see an annual peak in October inflation, then there will be a pullback in annual inflation with the base effect that will start to work. However, it is difficult to think that this effect will indicate a disinflationary process other than the base effect. We expect inflation to peak at 87.4% in October (our monthly forecast is 4.6%), rising from 83.5% in September before slowing down due to base effects. This rate will be exactly 17.5 times the 5% medium-term target of the CBRT.

Inflation is in a high and broad-based course. In October, we expect the general upward effect to continue in both volatile items and core groups. This, of course, will be multiplied by the effect of food and energy prices, and the deterioration in inflation expectations and pricing behavior will cause a rollover effect. Of course, this pricing and deterioration in expectations, which causes inflation inertia, is the primary risk that will cause disinflation to run slower and later than expected.

The declines observed in commodity prices as of October could have opened a comforting area for the headline CPI. On the other hand, Brent oil price remains high in October, and Russia’s suspension of the grain deal poses a global risk to food prices. Supply-based uncertainties are still very high, and this, of course, may cause an inflation stemming from global prices to be imported from the outside world in the coming period. The factor that may form the basis for the expectation of a decrease in global commodity prices is, of course, the effect of falling demand due to the recession. Here, it is still unclear at which supply-demand level the equilibrium point will occur and in which direction it will dictate prices.

The effect of food prices is also prominent in inflation indicators that we can take the lead. The ITO data released yesterday revealed that the prices in Istanbul rose by 3.96% in October and the annual increase in retail prices was 118.8%. Since Istanbul can be characterized as the commercial capital of Turkey, it is normal for prices to be higher than the general Turkish level. In the series from 2004, a correlation coefficient of 0.98 is reached in the annual inflation data of ITO and TURKSTAT. In this context, we can say that the monthly 4.6% and annual 87.4% inflation rates that we expected in October are in line with these indicators. The deviation may come from food prices, as ITO data shows a monthly increase of 5.5% (above the headline) in October. In Türk-İş data, another private inflation indicator, this food inflation was given as 2.5% per month. We consider the risks of food inflation to be upwards in the coming months due to the adverse developments in global grain prices and winter conditions.

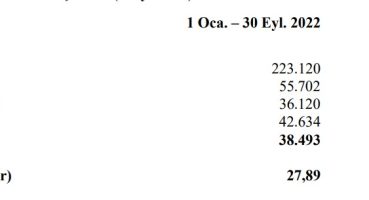

Main spending groups and headline CPI comparison. Source: Bloomberg, TurkStat, Tera Yatirim

We see and evaluate inflation as broad-based and consider it to be the most important risk for it to become permanent. On the basis of CPI, the prices of almost no products have shown a decline in recent months. Price increases will probably continue to occur on a periodic basis, especially in the agriculture and energy group, and this will have the effect of both global supply uncertainties and local economic/monetary policies. The accumulated cost effects in the PPI, the transition effect of Brent oil prices to fuel, deteriorating inflation expectations and the continuing demand effect due to unstable pricing will be the explanatory variables of the widespread inflation increases. We evaluate the general inflation trends as upwards, not only on the headline but also on the core basis.

Inflation, which we expect to peak in October, will lose momentum on an annual basis after this period, due to the base effect of the high realizations stemming from the lira crisis at the end of 2021 and the energy crisis in the first half of 2022. Compared to the 65.2% projection announced by the CBRT on October 27, we see the year-end inflation as 77.6%. We calculate the inflation, which we expect to decrease to 66.9% in January 2023 with the base effect, as 37.9% by the end of next year (CBRT 2023 forecast is 22.3%). These projections are related to our prediction of a slower disinflation.

If we look from the point of view of the CBRT; Despite high inflation, the Central Bank lowered interest rates by 350 basis points in its last three meetings. The central bank also signaled a new rate cut at its next meeting. We consider that the loosely grounded monetary and fiscal policies may weaken the lira and increase inflation. For this reason, we consider the disinflation area to be limited after the deceleration of inflation due to base effects, and we think that a strict inflation outlook will remain valid.

Kaynak: Tera Yatırım-Enver Erkan

Hibya Haber Ajansı